13 April 2026

During the latest tightening episode, interest rate hikes were especially effective. This ECB Blog finds a strong policy transmission to inflation during 2022 and 2023, a forceful response to supply-driven shocks and a low “sacrifice ratio”.

The effects of monetary policy in the euro area differ across countries, sectors and time.[1] These differences depend on prevailing economic conditions, and, crucially, on the nature of unexpected events which affect the economy. In this blog post we investigate the effects of the ECB’s interest rate increases over the period 2022-23, which curbed the inflation surge. It also compares these effects with those of previous interest rate changes.[2]

Effects of monetary policy over time

Monetary policy transmission in the euro area has evolved markedly over time. Recent model-based analysis reveals that while it reduced inflation, the increase in interest rates during the period July 2022 to September 2023 caused a relatively small contraction in economic activity. To illustrate this, we assess the effects of policy interest rate hikes through the lens of a structural autoregressive (SVAR) model. We use a time varying framework, meaning we apply this model to the euro area quarter by quarter over two decades. One can imagine this as a test in a model world designed as realistically as possible based on real life data.

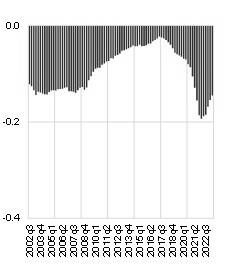

Chart 1 shows the time-varying peak responses of real gross domestic product (GDP), inflation measured through the Harmonised Index of Consumer Prices (HICP) and inflation expectations to a standard monetary policy shock normalised to +25 basis points. Such a shock is defined as an unexpected one-off increase in the interest rate at each point in time. Our model-based estimates show a pronounced strengthening of the inflation response to an interest rate hike over the period 2022-23, alongside a lower than usual response in terms of real activity.[3] A main driver of this result is how people’s expectations about future inflation behave. Even as inflation rose sharply from mid-2021, expectations remained firmly anchored. As monetary tightening accelerated from mid-2022 onwards, our analysis shows that there was a substantially stronger reaction in terms of inflation expectations than in earlier periods. This reinforced the disinflationary effects of the policy.

Chart 1

Accumulated effects over time of monetary policy on real GDP (left-hand panel), HICP inflation (middle panel) and one-year ahead inflation expectations of the ECB Survey of Professional Forecasters (right-hand panel)

(percentage points)

|

a) Effects on real GDP |

b) Effects on HICP |

c) Effects on inflation expectations |

|

|

|

Source: ECB and ECB staff computations.

Notes: The figures show peak responses (in percentage points) from impulse response functions estimated using a time-varying parameter SVAR over the period 2002 Q3 to 2023 Q3. The monetary policy shock is normalised to generate a 25-basis-point increase in the three-month EURIBOR (euro interbank offered rate) in the second period, ensuring that the estimated effects are comparable over time.

Does the nature of underlying shocks matter?

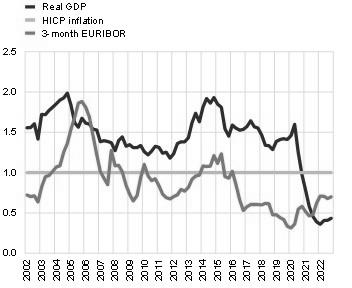

The economic responses to monetary policy decisions depend on the state of the economy and on the shock determining that state. Further analysis also confirms that the nature of the underlying shock hitting the economy matters for the monetary policy reaction. It makes a huge difference whether a shock is driven by supply or demand forces. The analysis points to a pronounced shift in the responsiveness of monetary policy to different types of shock in the post-pandemic period. In particular, results point to a markedly stronger reaction by the ECB to supply-driven inflationary pressures relative to earlier tightening episodes, such as 2006-2008. Chart 2 shows how aggregate demand and oil supply shocks affect real GDP, HICP inflation and the three-month EURIBOR (euro interbank offered rate) rate over time.

The reaction of the three-month Euribor shown in Chart 2, panel b) indicates that during the 2022-23 tightening episode, monetary policy responded more forcefully to aggregate supply shocks, such as energy and oil price shocks. This more decisive reaction reflects the fact that the pass-through from oil price disturbances to headline inflation substantially increased after 2022 compared with past episodes (Chart 2, panel b). This raised the risk that a temporary rise in inflation could become embedded in inflation expectations, thus requiring a more aggressive monetary policy response in comparison with past energy price surges.

Chart 2

Time-varying effects of shocks

(percentage points)

|

a) The effects of aggregate demand shocks over time |

b) The effects of oil supply shocks over time |

|

|

Source: ECB and ECB staff computations.

Notes: The figures show peak effects (in percentage points) from impulse response functions to an aggregate demand and an energy price shock obtained via time-varying parameter SVAR over the period running from 2002 Q3 to 2023 Q3. The aggregate demand shock has been normalised to generate a 1-percentage point peak increase in HICP inflation, while the oil price shock has been normalised to induce a 10-percentage point peak increase in the Brent oil price, allowing the estimated elasticities to be comparable over time.

Put simply, these results confirm that a stronger monetary policy response contains possible second-round effects more successfully, because it helps stabilise inflation expectations. This is key to reinforcing the disinflationary impact of monetary tightening.

State dependence and the sacrifice ratio

The results so far show that both the strength of monetary policy transmission and the policy reaction itself changed markedly over time. This was the case especially during the high-inflation episode of 2022-23. Does this reflect a change in the behaviour of monetary policy only? Or is it also the result of the economy responding differently to economic shocks for a given monetary policy reaction? More specifically, did the inflation-output trade-off change when inflation was high?[4]

Recent research shows that price and wage-setting behaviour is not constant but depends on the inflation environment. When inflation is low and stable, firms and workers adjust prices and wages infrequently. Also, inflation responds gradually to changes in economic conditions. When inflation is high, by contrast, adjustments become more frequent. This makes inflation more responsive to both shocks and monetary policy actions.

The above indicates an important non-linearity in inflation dynamics that is largely absent in standard linear models. This “state dependence” has important implications for the cost and effectiveness of monetary policy. A simple way to capture this is through the “sacrifice ratio”. What sounds like a religious practice is actually a concept used to measure the cumulative output loss required to achieve a given reduction in inflation. The analysis shows that the sacrifice ratio varies systematically with the inflation environment. In other words, during a period of high inflation the central bank might raise interest rates more forcefully, but – per percentage point decrease in inflation – the resulting loss of output is smaller relative to a policy interest rate hike during times of low inflation.

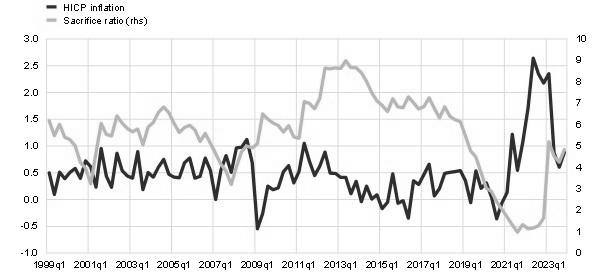

Chart 3

HICP inflation and “sacrifice ratio” over time

(quarterly changes and percentage points)

Source: ECB and ECB staff computations based on Ascari et al. (2025)

Notes: The sacrifice ratio is computed as the sum of output-gap deviations divided by the sum of inflation deviations over 20 quarters in response to a +0.25% unexpected monetary policy shock on the quarterly policy rate. HICP inflation expressed in quarterly growth rates.

As illustrated in Chart 3, higher underlying inflation levels are associated with lower sacrifice ratios. This indicates that monetary policy is more effective at reducing inflation when inflationary pressures are higher. Strikingly, under the assumption of anchored inflation expectations, the model suggests that in 2022 the sacrifice ratio was almost twelve times smaller than in 2012. This highlights the combination of greater price and wage flexibility during the recent tightening episode.

Together, the above findings help explain why it was possible to achieve the recent disinflation with relatively limited overall output costs. They also underscore how crucially the effectiveness of monetary policy depends on the inflation regime.

Conclusion

This blog post shows that monetary policy in the euro area was particularly effective during the 2022-23 tightening episode. It achieved rapid disinflation with limited output costs. This reflects a stronger transmission to inflation relative to past monetary policy interventions, a more decisive monetary policy response to supply-driven shocks, and the continued anchoring of inflation expectations.

Crucially, the analysis highlights that the effectiveness of monetary policy depends on the inflation environment. When inflation is high, prices and wages adjust more flexibly, making it easier to bring inflation down without large overall output losses. Overall, these findings underscore the importance of accounting for time variation, non-linearities and shock-specific dynamics when assessing monetary policy in high-inflation environments.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site