21 April 2026

Artificial intelligence (AI) can help track inflation risks in real time. A new ECB model based on machine learning informs experts how likely it is that inflation will be much higher or much lower than they expect.

In times of growing economic and political uncertainty, prices can change more rapidly and more strongly. This is why monetary policy decisions rely not only on the most likely path for inflation, which economists like to call the “baseline”, but also on an assessment of the risks surrounding it.[1] In other words, how likely it is that inflation will turn out to be higher or lower than the baseline. Estimating this has become much more complicated in a world of growing uncertainty. This blog post shows how the ECB is applying new AI-based tools to cope with this increased complexity.

The Eurosystem (the ECB and the national central banks of the euro area countries) utilises a comprehensive toolkit to analyse the risks surrounding inflation forecasts.[2] For example, market-based sensitivity analysis focuses on how surprise developments in key economic variables, such as oil prices, would affect the euro area economy. In addition, model-based analysis examines how a wide range of potential developments could shape the entire distribution of future macroeconomic outcomes. This offers a broader perspective than the sensitivity analysis. However, the standard economic models used in this context are typically based on only a handful of economic indicators. They may also rely on restrictive assumptions.[3]

The machine learning model described in this blog post comes with two major advantages for the risk analysis.[4] First, it is able to handle a greater number of economic indicators. Second, machine learning models are able to capture very general and complex data patterns. This allows it to detect and cope with non-linearities, which more traditional economic models often exclude.[5],[6]

Machine learning to assess inflation risk

The machine learning tool we use to assess the risks surrounding future inflation is based on a quantile regression forest (QRF) model.[7] It serves a dual purpose. First, it produces inflation forecasts. Second, it provides a comprehensive assessment of the risks surrounding a given baseline outlook, drawing on a large set of economic variables that are routinely monitored by Eurosystem inflation experts.[8] The model produces outputs based on the historical experience on which it has been trained and the most recent data available on key inflation determinants, such as wage developments and selling price expectations.

The ECB has already used the QRF model to help produce the short-term inflation forecast and the risk assessment around the baseline. Since the end of 2022, the model has become part of the broader analytical toolkit used for monetary policy preparation.[9]

Importantly, the potential of the QRF model extends beyond forecasting, and it can help identify which factors drive inflation risks over time.[10] In 2025, for example, wages and selling price expectations were the key forces behind revisions to our projections for core inflation (HICPX).[11]

Risk signals in real time

In recent years, the insights from the QRF model have been especially relevant. In particular, the model was useful in detecting – in real time – emerging inflation risks across different components of our main inflation measure (HICP). This made a tangible difference, because the volatile environment after the pandemic made it much harder to interpret the potentially conflicting messages emerging from the large number of indicators that we traditionally monitor for our analysis. Traditional economic models struggled with these conflicting messages, but QRF helped us to make sense of them.[12]

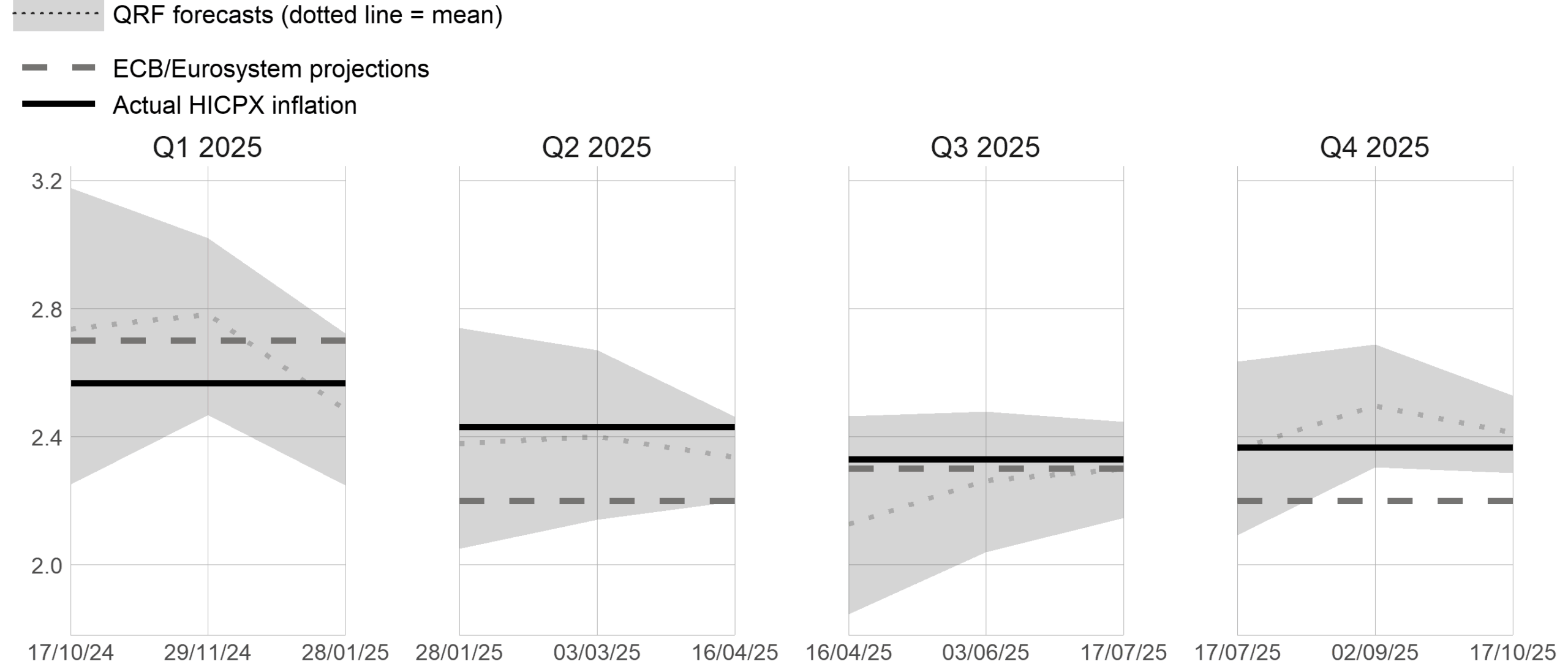

In the following, we focus on the performance of the QRF model in the course of 2025, comparing it to the ECB/Eurosystem projections produced around the same time.[13] The shaded area in Chart 1 captures the QRF density forecasts prepared on selected dates around each ECB Governing Council meeting held during the sample period. This shows the range in which HICPX inflation is likely to fall according to the model. For example, the QRF forecasts for the first quarter of 2025 were produced on 17 October 2024 and updated on 29 November 2024 and 28 January 2025 as more information became available. The ECB/Eurosystem projections for HICPX inflation for each quarter of 2025 are shown by the dashed red line. For all quarters displayed, the projections are prepared using the information available on the mid-date of the range reported on the x-axis. Finally, the actual outcome, which is generally released soon after the end of the reference quarter, is shown by the solid black line.

Chart 1

Core inflation projections in 2025

(percentages)

Source: ECB staff calculations. Notes: The chart compares ECB/Eurosystem projections with selected vintages of QRF density forecasts for core inflation around relevant Governing Council meetings. The QRF model is based on Lenza et al. (2025). The shaded areas represent the 16th and 84th percentiles of the QRF forecasts, the dotted line represents the mean forecast.

How big risks around the ECB/Eurosystem baseline inflation projections are can be derived from how far the QRF analysis deviates from the ECB/Eurosystem projections. For example, if the ECB/Eurosystem projection falls in the lower part of the shaded area, or even outside its lower range, the projection carries an “upside risk”, i.e. the QRF analysis identifies a considerable likelihood that the final outcome for inflation will be higher than predicted. Comparing the QRF-based risk signals with how actual inflation subsequently turned out suggests that these signals were informative. For example, for the second and fourth quarters of 2025, the QRF range lies mostly or entirely above the ECB/Eurosystem projections and inflation was indeed 20 basis points above the projections. Hence, the upside risks identified by the model did materialise. At the same time, when the projections were closer to the mid-point of the range (indicating that no meaningful risks were detected by the model), the projections turned out to be more in line with the final outcomes. The shaded area of the QRF model area shrinks in the course of each quarter while, at the same time, still generally encompassing the final outcome. This shows that the QRF predictions become more precise as new information becomes available over the course of the quarter.

Implications for economic and inflation analysis and the road ahead

The examples above show that the QRF model is a helpful tool to navigate uncertain macroeconomic conditions. The ECB’s experience in developing and exploiting this model points the way for future uses. First, machine learning tools can complement traditional models by providing timely information about risks, including their magnitude, orientation and determinants. Second, these new tools are valuable not only for their forecasting accuracy but also for their ability to reveal complex data patterns, such as non-linearities and sector-specific dynamics, that have become increasingly relevant for monetary policy in recent years.

The QRF framework also allows growing data volumes to be handled more efficiently. This makes it possible to assess economically interpretable risk in real time, which in turn allows changes in the baseline or the associated risks to be detected swiftly. The QRF analysis provides explanations of how key variables of interest, such as inflation or output, evolve based on the evolution of their core determinants (e.g. wages, import costs or expectations). Hence, we believe these new tools will play a growing role in forecasting, monitoring economic and inflation trends, and informing monetary policy decisions.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site