15 May 2026

Non-bank financial institutions (NBFIs) are on the rise. This blog shows how shifts in their borrowing and investment portfolios constrain financing for euro area firms and affect the transmission of monetary policy.

Two trends have diverted financing away from euro area firms in recent years. First, euro area NBFIs have shifted their portfolios towards foreign assets – particularly US equities. Second, banks have channelled more lending to NBFIs outside the euro area. Together, these cross-border flows via NBFIs contributed to a sluggish recovery in firms’ external financing over recent years.

NBFIs are reshuffling their portfolios at the expense of euro area firms

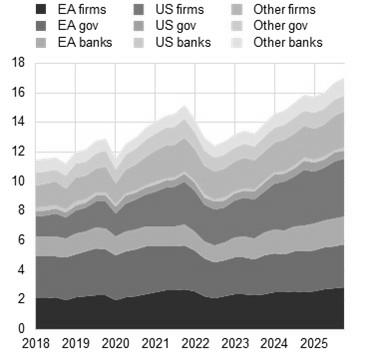

NBFIs, such as investment funds and insurers, play a crucial role in financing firms through both equity and bond markets. In recent years, euro area NBFI securities holdings have grown substantially, rising from around €11 trillion in early 2018 to €17 trillion by the end of 2025 (Chart 1, panel a). Investment funds account for roughly 60% of the total.[1] Strikingly, however, the composition of these portfolios has been shifting away from European assets more recently.[2]

Most of this reflects the exceptional performance of US stocks – especially in the tech sector. This has systematically raised their value relative to European holdings. But the changing composition of NBFIs’ portfolios is not just a valuation story: NBFIs, particularly investment funds, do not just hold US equities, they have also been buying them.

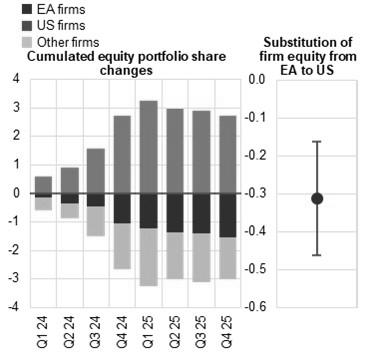

Since late 2023 euro area NBFIs have increased their allocation to US corporate equities by around 2.7 percentage points through net purchases. At the same time, they have reduced their allocation to euro area corporate equities by about 1.5 percentage points (Chart 1, panel b, left). The reallocation has come, to a lesser extent, at the expense of euro area government bonds and bank equities.

Chart 1

Developments in NBFI equity and debt portfolios

|

a) NBFI debt and equity holdings, by issuer sector and geography |

b) NBFI holding of firm equity |

|---|---|

|

EUR trillion |

percentage points |

|

|

Source: ECB (SHSS), ECB calculations and Henricot, D., Mendicino, C., Molestina Vivar, L. and Pelizzon, L. (2026).

Notes: For panel a) amounts are in market value. The holdings are for euro area NBFIs (ICPF, IF, MMF and OFIs). For panel b), left-hand scale, the chart shows NBFIs’ cumulative transaction-based firm equity portfolio share changes for NFCs in the euro area, the United States and other countries in relation to the fourth quarter of 2023. NBFIs include ICPFs, IFs, MMFs, and OFIs. The right-hand scale is based on a coefficient from a regression of euro area NFC equity shares on US NFC equity shares in euro area NBFI portfolios, based on sector-level data and controlling for NBFI sector and quarter fixed effects (2014-25).

The latest observations are for the fourth quarter of 2025.

These developments clearly matter for the financing of euro area firms. Research by Henricot, Mendicino, Molestina Vivar and Pelizzon finds that increases in the share of US corporate equities in NBFI portfolios are associated with declines in the share of euro area equities. An increase of 1 percentage point in the share of US equities in NBFI portfolios is associated with a 0.3 percentage point reduction in the share of euro area corporate equities (Chart 2, panel b, right).[3] While the substitution effect is not one-for-one, it is meaningful and material. And it suggests that the growing appetite for US assets may be squeezing out equity financing for European businesses.

Banks are lending more to non-bank financial institutions and less to firms

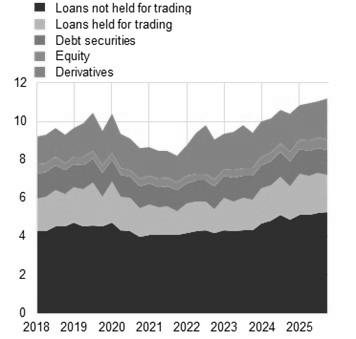

A similar dynamic is playing out on the banking side. Bank exposures to NBFIs have grown steadily in recent years, reaching around 11% of total assets by the end of 2025 (Chart 1, panel a).[4] Most of this takes the form of direct loans predominantly to investment funds and other financial institutions – mainly short-term collateralised loans (reverse repos). A substantial share of these loans is directed to entities operating outside the euro area.[5]

Chart 2

Bank loans to non-banks and firms

|

a) Bank asset-side exposure to NBFIs |

b) Bank loans to non-banks and firms |

|---|---|

|

percentages of total assets |

LHS: percentage points; RHS: coefficient |

|

|

Source: For panel a) ECB (Supervisory Reporting) and ECB calculation; for panel b) ECB (Supervisory Reporting, AnaCredit), Orbis, ECB calculations and Li, Ma, Mendicino, Supera (2025).

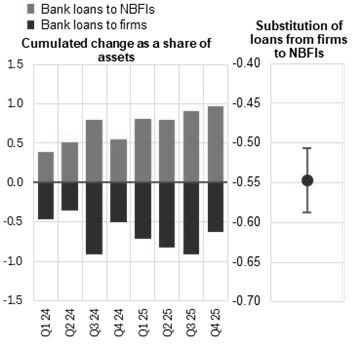

Notes: Panel b), left-hand scale, shows cumulated change relative to the fourth quarter of 2023. NBFIs stands for non-bank financial institutions. Bank loans exclude loans held for trading. The sample consists of a balanced sample of significant institutions reporting under IFRS. The right-hand scale is based on a coefficient from a regression of firm borrowing, on the dynamics of bank lending to NBFIs by each firm’s relationship banks, between 2019-25.

The latest observations are for Q4 2025.

It is especially notable that this trend has come at the expense of lending to firms (Chart 1, panel b).[6] Research by Li, Ma, Mendicino and Supera shows that when the bank a firm borrows from increases its NBFI lending by 1 percentage point, that firm’s access to bank credit falls by 0.55 percentage points on average (Chart 1, panel b). Crucially, firms cannot easily make up the shortfall by turning to other banks or NBFIs for alternative funding.[7]

In the current geopolitically uncertain environment[8], reverse repos to NBFIs are an attractive option for banks, particularly those with weaker capital positions. It is therefore unsurprising that this expansion aligns with the risk-averse attitudes banks have reported in recent surveys.[9]

Conclusion

The two trends described in this post point in the same direction: cross-border flows via NBFIs weigh on the recovery of firm financing over the ECB’s easing cycle.

When euro area investment funds reshuffle their portfolios in favour of US equities, European firms find it harder to raise capital in markets. When banks shift towards foreign NBFIs over domestic borrowing firms, European firms find it harder to secure loans. The result is a sluggish financing recovery that is lagging behind policy rates.[10] This is a reminder that as NBFIs grow in global importance their cross-border behaviour deserves close and sustained attention from policymakers.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe to receive future posts via email.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site