24 June 2026

The adoption rate of AI is rising rapidly, but the intensive use that drives transformation and generates macroeconomic gains remains rare. This blog explores what sets intensive AI users apart and what firms need to deeply integrate AI into their production processes.

The advent of AI has been widely hailed as a driver of productivity growth. Yet simply adopting AI does not guarantee measurable improvements in firms’ efficiency. What does matter is what they use the new technology for. Firms that apply AI to core processes tend to generate more value than those that restrict its use to peripheral or routine tasks. Intensive use, meaning use that goes beyond infrequent or moderate levels, particularly when linked to innovation and the expansion of products and services, is more likely to boost productivity and support economic growth.

So far, however, very few firms in the euro area actually use AI intensively. Understanding what differentiates intensive users from other firms and what enables them to fully leverage AI is therefore essential. To that end, we took a closer look at the ECB’s Survey on the access to finance of enterprises (SAFE).

AI diffusion continues to rise, but deepening takes time

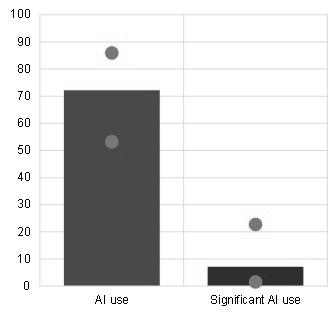

How large is AI’s footprint so far? As SAFE – our survey of over 5,000 firms across euro area countries – and other recent studies show, diffusion is increasing quickly. In the last quarter of 2025, more than 70% of firms reported using AI (Chart 1, panel a), a trend that looks set to continue. Nearly half of the firms that were not using AI in 2025 plan to invest in it in 2026.

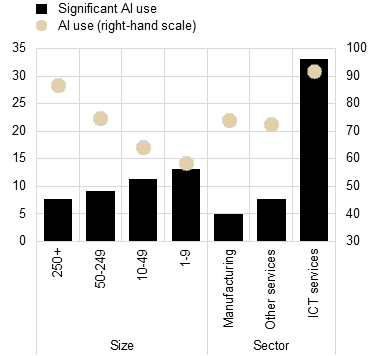

At the same time, most firms report using AI only infrequently or moderately, with only 7% of euro area firms reporting intensive use. There are, however, considerable differences across countries, sectors and firms. While the likelihood of adopting AI increases with firm size – this has been well established in the literature[1] – intensive use is relatively more common among small firms (Chart 1, panel b). Younger firms – those active for less than ten years – also report intensive use more frequently than older firms. Overall, however, it is size rather than age that appears to be more closely associated with intensive AI use.

The line of business also makes a difference. Intensive use is particularly prevalent in services, especially – and unsurprisingly – in high-tech, knowledge-intensive services like the information and communication (ICT) sector. These sectors include developers and providers of AI tools, which tend to be highly digitalised. They also have access to abundant data and computing infrastructure and employ workers with strong technical skills.

Chart 1

AI use and intensity

|

a) Use and intensive use of AI |

b) Use and intensive use of AI by firm size and sector |

|---|---|

|

(percentage of firms) |

(percentage of firms) |

|

|

Source: ECB Survey on the access to finance of enterprises, round 37 (October-December 2025).

Notes: Panel a) shows the weighted share of firms using AI and using AI intensively. Red dots represent the smallest and the highest weighted average for countries. Panel b) shows the weighted share of firms using AI intensively out of all firms using AI for employment-based size classes, manufacturing, information and communication services and other services. Detailed sector information is from Orbis. Intensive use refers to responses indicating “significant use” when assessing the adoption of AI technologies by the firm.

Why do firms use AI? The reasons differ among intensive and moderate users. Firms at an early stage of adoption often cite cost reductions and improvements in operational efficiency as their main reasons for using it. By contrast, intensive users are more frequently motivated by growth and innovation. Responses to the SAFE survey show that intensive users are more likely to mention employment growth[2], as well as support for research and development. They also mention the expansion of products and services as key reasons for adopting AI.

Intensive use driven by peer pressure

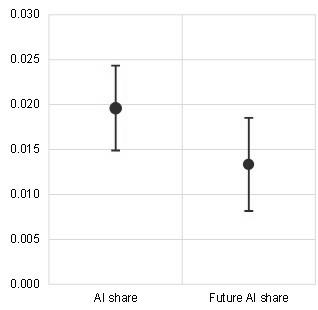

Beyond firm and sector factors, survey results indicate that peer pressure is a key driver of intensive AI use. When firms see their peers investing in AI, they fear a potential competitive disadvantage and therefore also feel the need to use the technology more intensively (Chart 2).

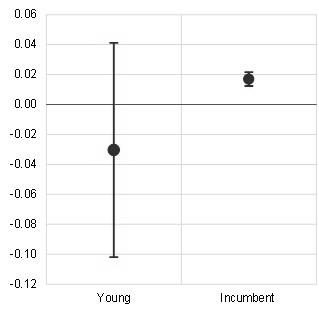

A similar pattern emerges when looking at expectations about the diffusion of future AI investment. Firms that expect a higher future share of AI users among similar-sized firms in their sector are likely to intensify their own use of the technology (Chart 2, panel a). The peer pressure effect is primarily driven by incumbent, well-established firms rather than young firms. This means that incumbent firms adopt AI more intensively as they feel threatened by young firms that are technologically advanced, as well as by their high-performing peers (Chart 2, panel b).

Chart 2

Impact of peer pressure on AI use: intensive versus moderate users

|

a) Current versus future peer pressure |

b) Peer pressure of young and incumbent firms |

|---|---|

|

(Average marginal effects) |

(Average marginal effects) |

|

|

Source: ECB Survey on the access to finance of enterprises, round 37 (October-December 2025).

Notes: Perceived AI use and expected future AI use refer to the current and future share of firms investing in AI in the same sector and size class as perceived by respondents. The charts report average marginal effects from firm-level regressions where the dependent variable is a binary dummy taking the value 1 for intensive AI use and 0 for moderate or infrequent AI use. A 10 percentage point increase in the current (future) AI investment rate increases the probability that a firm is AI-intensive by about 1.9 (1.4) percentage points. Young firms are firms that are less than five years old. Survey-weighted regressions with industry, country, firm size and age fixed effects. Whiskers represent 90% confidence intervals.

The peer pressure effect is most pronounced in ICT and professional services. These sectors have a high share of young firms, a large presence of high-growth firms and exposure to technologically advanced foreign competitors. Taken together, these features indicate highly dynamic and competitive business environments. In these settings, incumbent firms are compelled to intensively adopt advanced technologies, such as AI, to remain competitive.

Table 1

Impact of peer pressure by sector and sectoral characteristics

|

Impact |

Sector |

Exporters |

Young |

High-growth |

|---|---|---|---|---|

|

High and significant |

J ICT |

|||

|

High and significant |

M Professional services |

|||

|

Low and significant |

H Transport |

|||

|

Low and significant |

F Construction |

|||

|

Insignificant |

C Manufacturing |

|||

|

Insignificant |

D Energy |

|||

|

Insignificant |

E Water & waste |

|||

|

Insignificant |

G Trade |

|||

|

Insignificant |

I Accommodation |

|||

|

Insignificant |

L Real estate |

|||

|

Insignificant |

N Admin support |

|||

|

Insignificant |

R Arts |

|||

|

Insignificant |

S other services |

Source: ECB Survey on the access to finance of enterprises, round 37 (October-December 2025), Eurostat.

Notes: Sectors are ranked based on their contribution to the peer-pressure effect and its statistical significance. The reported impact represents average marginal effects from firm-level regressions, where the dependent variable is a binary indicator equal to 1 for intensive AI use and 0 for moderate or infrequent AI use. Exporters denotes the share of exporting firms (based on the SAFE sample). Young denotes the share of firms less than five years old (SAFE sample). High-growth denotes the share of high-growth firms in the sector (based on Eurostat data). Green indicates sectors with above-median values of the respective characteristic; orange indicates sectors with below-median values.

Intensive AI use requires broader financing

The SAFE results also show that more than 84% of firms reporting intensive AI use have invested in the technology. Only 33% of moderate users, however, have done so. Looking ahead, 99% of intensive users plan to invest in AI in 2026, allocating around 20% of their total investment to AI-related activities.

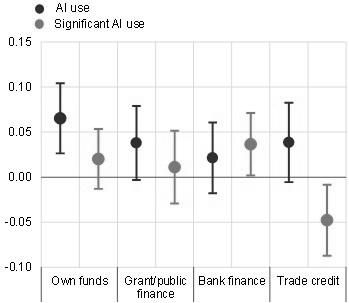

This shows that investments that go beyond purchasing licences for general AI tools typically require more substantial funding. Indeed, integrating AI into core processes, such as developing customised solutions or upgrading digital infrastructure, often entails larger and longer-term restructuring. And these investments cannot easily be financed through short-term instruments such as trade credit or own funds.

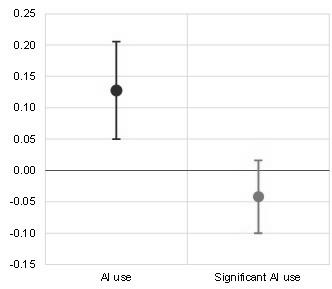

Our analysis comparing firms in the same industry and country, and of similar size and age, shows that firms using AI intensively are more likely to combine several sources of financing. In the euro area, companies have fewer ways to raise money directly from investors or financial markets, so they depend more on bank loans to finance AI investments (Chart 3). This contrasts with findings that compare AI users with non-users, where firms using AI are more likely to rely on own funds compared with firms not using AI.

Interestingly, it also matters who the company owners are. As our statistics show, firms with public shareholders are more likely to adopt AI. This could reflect a greater willingness of professional management to adopt new technologies. However, being publicly owned does not mean a company is more likely to go from moderate to intensive AI use.

Chart 3

Impact of financing and ownership on intensive use of AI

|

a) Impact of various financing sources |

b) Impact of market ownership |

|---|---|

|

|

Source: ECB Survey on the access to finance of enterprises, round 37 (October-December 2025).

Notes: Panel a) indicates whether firms view each financing source as relevant. A financing source is considered relevant if the firm used it in the past or is considering using it in the future. Panel b) indicates whether firms are owned by public shareholders (i.e. listed firms) or report other types of ownership. The charts report average marginal effects from firm-level regressions, where the dependent variable is a binary dummy taking the value 1 for intensive AI use and 0 for moderate or infrequent AI use. Survey-weighted regression with industry, country, firm size and age fixed effects. Whiskers represent 90% confidence intervals.

What can help firms intensify their AI use?

As shown above, only a fraction of firms use AI intensively. The macroeconomic impact of AI will depend on whether firms move beyond initial experimentation and begin using the technology intensively in their core activities. So, what do firms need to expand their use?

Here, it is important to look beyond the broader structural constraints such as competitive pressure, market dynamism and access to financing. Unsurprisingly, the survey results suggest that technological factors matter. Firms most often cite shortages of AI-related skills (40%), limited usefulness of current AI technologies for their business needs (28%) and incompatibility with existing systems (26%).

Targeted policy support could help address some of these issues. In particular, it could help small and medium-sized enterprises scale up their efforts. Promoting the sharing of successful use cases could, for instance, help raise awareness of AI’s potential. Furthermore, applied training programmes for managers, employees and IT specialists, together with subsidised advisory services, could also help firms strengthen the skills needed to implement AI effectively.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe to receive future posts via email.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site