26 May 2026

The economic shock caused by the war between the United States and Iran has quickly fed into euro area firms’ expectations. Daily responses to an ECB survey show an immediate increase in expected input costs, selling prices and short-term inflation.

Firms’ expectations for costs, prices and the broader macroeconomic environment are central to their decisions on wages, investment and employment. These decisions, in turn, determine how economic shocks are transmitted to the economy. When a major geopolitical event occurs, a key question for central banks is how quickly and how persistently the shock will feed into firms’ expectations. For monetary policy, it is essential to understand whether the adjustment to the shock is a short-lived supply disruption or a longer-lasting change that might lead to medium-term inflationary pressures.

The latest round of the ECB’s Survey on the Access to Finance of Enterprises (SAFE), offers a rare opportunity to study exactly this question. The survey for the first quarter of 2026, carried out between 19 February and 1 April, spans the period including the outbreak of the war in the Middle East on 28 February. What makes the survey results particularly interesting is the fact that the interviews with firms were carried out in different weeks throughout this period. This makes it possible to compare the answers of firms interviewed before and after the start of the conflict. Thereby, it provides evidence for the way the geopolitical shock has been transmitted to firms’ expectations.[1] Most strikingly, the results indicate an immediate increase in expected input costs, selling prices and short-term inflation.

Impact on costs and selling prices one year ahead

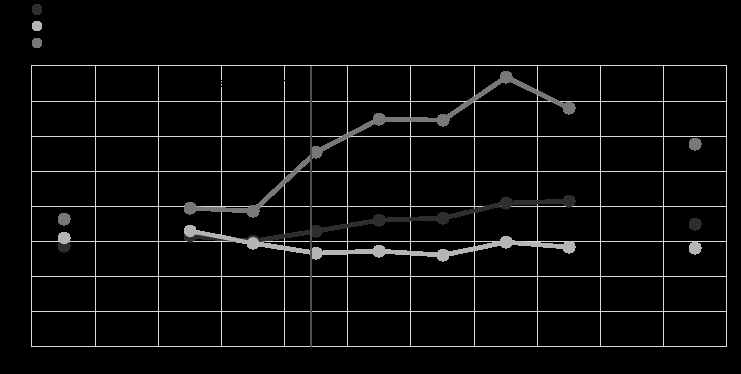

Chart 1 provides a first glimpse of the impact of the war on euro area firms’ expectations for costs and selling prices over the next 12 months. It displays weekly averages of SAFE responses collected before and after 28 February 2026, and points to a clear shift in sentiment. In the two weeks prior to the outbreak of the war, firms expected their selling prices and non-labour input costs to increase on average by 3.0% and 3.9% respectively. These figures were broadly in line with those in the previous survey round (2.9% and 3.6%).[2] This suggests that without the war, expectations would likely have remained on a similar, stable path.

Chart 1

Expectations for selling prices, wages and input costs one year ahead, before and after the outbreak of the war in the Middle East

(percentage changes over the next 12 months)

Sources: Survey on the Access to Finance of Enterprises and authors’ calculations. Notes: The chart shows average expectations of firms over the following 12 months, before and after the outbreak of the war in the Middle East. The survey results are aggregated on a weekly basis.

Following the outbreak of the war, however, both cost and price expectations rose markedly. For firms surveyed after 28 February, weekly averages climbed progressively, reaching a peak of 4.1% for the expected change in selling prices and 7.7% for input costs in the final weeks of the collection period. This pattern mirrors the sharp and sizeable rise in energy prices at that time and the intensification of the conflict. Wage cost expectations, by contrast, moved modestly in the opposite direction, declining from 3.0% before the outbreak to 2.8% afterwards.

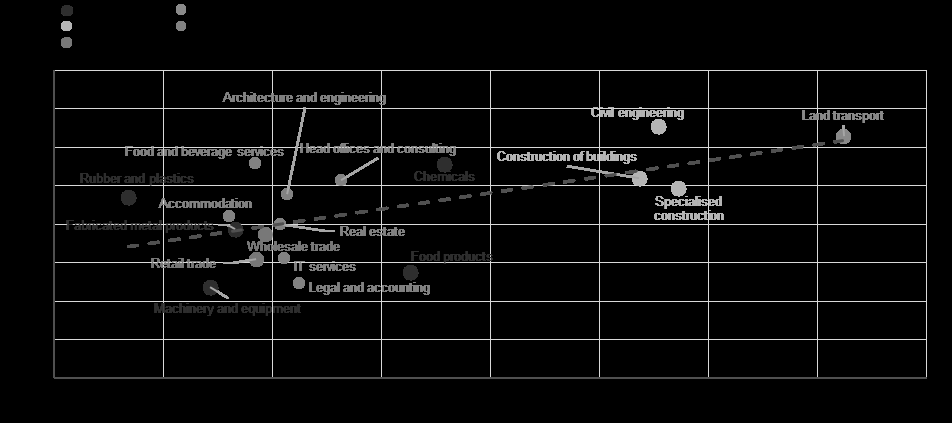

The rise in input cost expectations was not the same in all sectors. Firms operating in industries that rely more on fossil energy anticipated the sharpest cost increases over the next 12 months. The largest increases were expected by construction and transportation, both with high fossil fuel consumption (Chart 2). This pattern suggests that revised expectations were closely linked to firms’ exposure to energy price fluctuations triggered by the war. It also raises the possibility that firms in energy-intensive industries may have made bigger adjustments to their expectations not only for costs but also for business activity and financing conditions – a result we explore in more detail later in the post.

Chart 2

The relationship between input cost expectations and fossil energy consumption

(x-axis: percentage of fossil energy in total energy consumption, y-axis: percentage change in input costs over the next 12 months)

Sources: Survey on the Access of Finance of Enterprises, Moody’s Orbis database, Eurostat industry energy consumption statistics and authors’ calculations. Notes: The chart shows survey-weighted average expectations of euro area firms for changes in input costs over the next 12 months, aggregated at the NACE 2-digit sector level. The sample includes only sectors with at least 100 firms that can be matched to the Orbis database. The horizontal axis shows the share of fossil energy in total energy consumption by sector, based on Eurostat industry energy consumption statistics.

Impact on inflation expectations

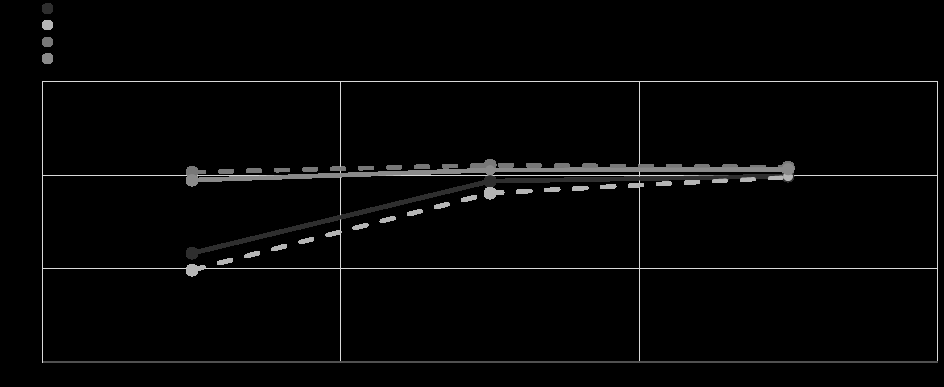

The war has also left a mark on the way euro area firms perceive the short-term inflation outlook. Chart 3 offers a straightforward way to read the impact of the war on inflation expectations for one, three and five years ahead. It compares the median inflation expectation reported by firms surveyed in the two weeks before the attack on 28 February with the median reported after that date. If the war had had no effect on inflation expectations, one would expect the two lines to overlap across the three horizons. Instead, the chart reveals a more nuanced picture. It shows a clear upward shift at the one-year horizon, while expectations for three and five years ahead are broadly unchanged. This indicates that firms currently see the impact on inflation as temporary.

The survey results bear this out. Firms interviewed before the outbreak of the war reported a median one-year ahead inflation expectation of 2.5%, almost unchanged from the previous survey round. Among firms surveyed after 28 February, this figure rose to 3.0%. This suggests that the war and the associated rise in energy prices and supply disruptions had prompted a substantial upward revision to short-term inflation expectations. Three-year and five-year ahead median inflation expectations, by contrast, were similar across the two groups. This indicates that firms did not, at this stage, expect the inflationary impulse to persist over the medium to longer term.

Chart 3

Firms’ inflation expectations before and after the outbreak of the war in the Middle East at different horizons

(annual percentages)

Notes: The chart shows survey-weighted median expectations for euro area inflation in one year, three years and five years’ time. “before the war outbreak” refers to SAFE survey data from the Q1 2026 round collected between 19 February and 27 February 2026, and “after the war outbreak” refers to Q1 survey data collected between 28 February and 1 April 2026.

Impact on expectations for near-term business activity and bank loan availability

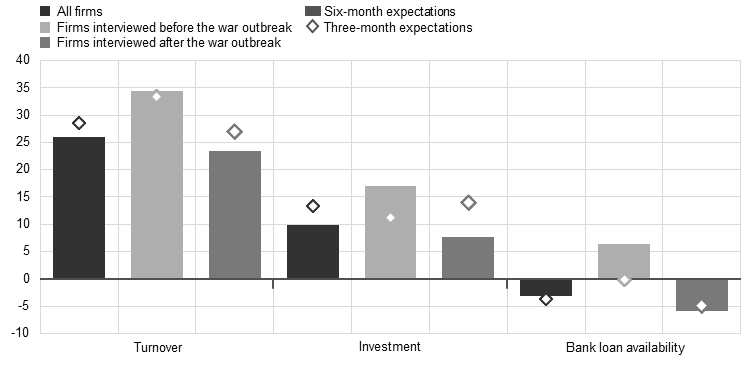

The impact of the war has not been confined to firms’ cost and price expectations. It has also dampened their short-term expectations for business activity and access to finance. Chart 4 compares the net percentages of firms expecting turnover, investment and bank loan availability to improve over the next three and six months between those surveyed before and after the outbreak of the war. Across all three indicators, firms interviewed after 28 February reported a noticeably more pessimistic outlook than those surveyed beforehand, consistent with the broader uncertainty brought by the conflict.

Chart 4

Firms’ expectations for business activity and bank loan availability over the next three and six months

(net percentages of respondents)

Notes: The chart shows survey-weighted net percentages of euro area firms’ expectations for changes over the next six months (bars) and over the next three months (diamonds), before and after the outbreak of the war in the Middle East. “Before the war outbreak” refers to SAFE survey data from the Q1 2026 round collected between 19 February and 27 February 2026, and “after the war outbreak” refers to Q1 survey data collected between 28 February and 1 April 2026. Net percentages are the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease.

The shift in firms’ expectations for credit conditions is particularly striking. Firms surveyed before the war anticipated, on balance, an improvement in bank loan availability over the coming six months, with a net 6% expecting conditions to ease. Among firms surveyed after the outbreak, sentiment had reversed, with a net 6% expecting the availability of bank loans to decrease. This reversal underscores the potential for geopolitical instability to make lenders more risk-averse. Unless the conflict is resolved quickly, it signals a challenging environment for firms seeking external financing in the near future. The chart also highlights differences between shorter-term (three-month) and medium-term (six-month) expectations. While firms reported a more pessimistic outlook for turnover and bank loan availability across both reference periods after the outbreak of the war, their investment plans deteriorated only at the six-month horizon. Expectations for three months ahead were broadly unchanged. Taken together, these findings suggest that the conflict has led firms to reassess their near-term business outlook, while adjustments to investment plans have so far remained more limited and concentrated at longer horizons.

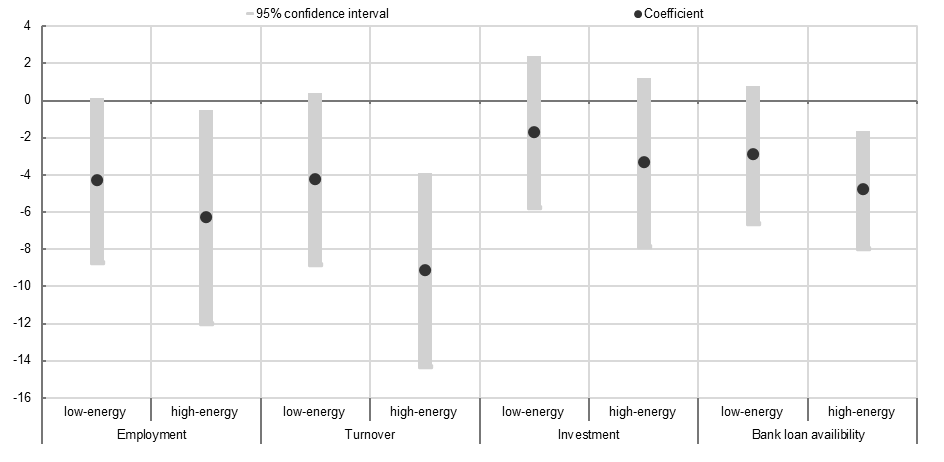

Energy-intensive firms become more pessimistic

The aggregate deterioration in firms’ expectations masks substantial differences across sectors. Chart 5 shows that the worsening of sentiment following the outbreak of the war was driven by firms in energy-intensive sectors, although the size of the change differs across expectation measures.

Chart 5

Change in expectations for employment, turnover, investment and bank loan availability by firms’ energy intensity

(percentage marginal probability of an increase in expectations)

Sources: Survey on the Access to Finance of Enterprises, Moody’s Orbis database, Eurostat industry energy consumption statistics and authors’ calculations. Notes: The chart shows the marginal effect of the coefficients from an ordered probit model for the outcome “increase” in expectations for employment, turnover, investment and bank loan availability. The coefficient measures the difference between the firms surveyed before and after the war in the Middle East, multiplied by a dummy for high-energy intensity sectors (energy consumption divided by gross value added above the median across countries and NACE 2-digit sectors). The regressions use survey weights and combine in the sample firms interviewed about their one-quarter and two-quarter ahead expectations. Expectations for employment are over the next 12 months.

For employment and turnover expectations, the adjustment among energy-intensive firms is statistically significant, particularly for turnover. By contrast, there is no significant effect on investment expectations over the next three to six months.[3] This suggests that energy-intensive firms have a less optimistic outlook for revenues as a result of the conflict and the associated rise in energy costs, but they have barely adjusted their investment plans for the time being. This may reflect the longer-term nature of investment decisions, as firms typically revise their plans only when a shock is perceived to be persistent. Overall, the concentration of the adjustment among energy-intensive firms provides additional indication that the geopolitical shock has mainly operated through the energy price channel.

Finally, the deterioration in sentiment has also extended to financing conditions. Energy-intensive firms became significantly more pessimistic about bank loan availability after the US-led attack on Iran. This suggests that rising energy costs and weaker expected profitability translated into concerns about future access to external financing, potentially reflecting a tighter supply of bank credit for firms facing cash flow constraints. This result points to a potential amplification mechanism, whereby energy price shocks not only weaken firms’ activity outlook directly but also by tightening expected financing conditions.

Conclusion

The pattern emerging across all four expectation dimensions collected in the survey – input and wage costs, selling prices, inflation expectations and business activity – bears the hallmarks of a supply-driven shock. Firms have revised up their short-term cost, price and inflation expectations while simultaneously marking down their near-term outlook for turnover, employment, investment and access to finance. Importantly, the deterioration in sentiment has been concentrated among firms operating in energy-intensive sectors. This highlights the central role of the energy price channel in the transmission of the shock. At the same time, the stability of wage expectations and longer-term inflation expectations suggests that, so far, firms do not anticipate the shock becoming persistent.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site